Backgrounder on Nuclear Insurance and Disaster Relief

On this page:

- Nuclear Insurance: Price-Anderson Act

- Price-Anderson in Action

- Onsite Insurance Requirements

- International Liability Agreement

Nuclear Insurance: Price-Anderson Act

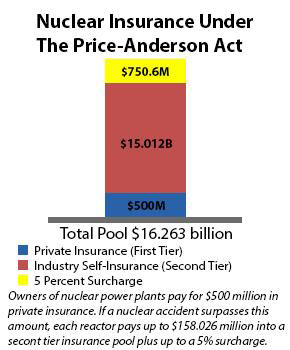

The Price-Anderson Act became law on Sept. 2, 1957, to cover liability claims of members of the public for personal injury and property damage caused by a commercial nuclear power plant accident. The legislation helped encourage private investment in commercial nuclear power by placing a cap, or ceiling, on the total amount of liability each nuclear power plant licensee faced in the event of an accident. Over time, the “limit of liability” for a nuclear accident has increased the insurance pool to more than $16 billion.

Currently, owners of nuclear power plants pay an annual premium for $500 million in private insurance for offsite liability coverage for each reactor site (not per reactor). This primary, or first tier, insurance is supplemented by a second tier. In the event a nuclear accident causes covered damages in excess of $500 million, each licensee would be assessed a prorated share of the excess, up to approximately $158 million per reactor. With 95 reactors currently in the insurance pool, this secondary tier of funds contains about $15 billion. (This figure reflects 94 operating reactors plus the San Onofre Nuclear Generating Station, Unit 1, which is still participating in the insurance pool.) Payouts of more than 15 percent of these funds require a prioritization plan approved by a federal district court. If the court determines that public liability may exceed the maximum amount of financial protection available from the primary and secondary tiers, each licensee would be assessed a pro rata share of this excess not to exceed 5 percent of the maximum deferred premium ($158 million); approximately $7.9 million per reactor. If the second tier is depleted, Congress is committed to determine whether additional disaster relief is required.

|

The only insurance pool writing nuclear liability insurance, American Nuclear Insurers, is comprised of U.S.-based property-casualty insurance and reinsurance companies. The average annual premium for a single-unit reactor site in 2025 is approximately $1.1 million. The premium for a second or third reactor at the same site is discounted to reflect a sharing of limits. The average site premium for 2025 is approximately $1.5 million. Claims resulting from nuclear accidents are covered under Price-Anderson; for that reason, all U.S. property and liability insurance policies exclude nuclear accidents. Claims can include any incident (including those caused by theft or sabotage) in transporting nuclear fuel to a reactor site; storing nuclear fuel or waste at a site; during operation of a reactor, including the discharge of radioactive effluent; and transporting irradiated nuclear fuel and nuclear waste from the reactor. Insurance under Price-Anderson covers bodily injury, sickness, disease or resulting death, property damage and loss, including reasonable living expenses for evacuated individuals. The Further Consolidated Appropriations Act of 2024 extended the Price-Anderson Act to Dec. 31, 2065.

|

Price-Anderson in Action

During the accident at the Three Mile Island nuclear power plant in Middletown, Pennsylvania, in 1979, the Price-Anderson Act provided liability insurance to the public. Coverage was available to those in need by the time Pennsylvania’s governor recommended the evacuation of pregnant women and families with young children living near the plant. At the time of the accident, private insurers had $140 million of coverage available in the first-tier pools. Insurance adjusters advanced money to evacuated families to cover their living expenses, requesting that unused funds be returned; recipients sent back several thousand dollars. The insurance pools also reimbursed more than 600 individuals and families for lost wages as a result of the accident.

The insurance pools were later used to settle a class-action suit for economic loss filed on behalf of residents who lived near the plant. The Price-Anderson Act also covered court fees. The last of the litigation surrounding the accident was resolved in 2003. Altogether, the insurance pools paid approximately $71 million in claims and litigation costs associated with the Three Mile Island accident.

![]()

Onsite Insurance Requirements

Although not required by the Price-Anderson Act, NRC regulations (10 CFR 50.54(w)) require licensees to maintain a minimum of $1.06 billion in onsite property insurance at each reactor site. The NRC added this requirement after the Three Mile Island accident out of concern that licensees may be unable to cover onsite cleanup costs resulting from a nuclear accident. This insurance is required to cover the licensee’s obligation to stabilize and decontaminate the reactor and site after an accident. Currently, only Nuclear Electric Insurance Limited provides this insurance for licensees.

![]()

International Liability Agreement

Separate from the Price-Anderson Act, the United States is a party to the Convention on Supplementary Compensation for Nuclear Damage, which was developed under the auspices of the International Atomic Energy Agency to be the basis for a global nuclear liability regime. The CSC provides an additional amount of liability coverage for nuclear incidents in the United States (currently up to approximately $57 million) resulting in damages in excess of the first-tier amount specified in the CSC. The CSC was adopted on Sept. 12, 1997. The United States signed at that time and deposited its instrument of ratification in May 2008. The CSC entered into force on April 15, 2015.

July 2025

![]()

Page Last Reviewed/Updated Wednesday, August 06, 2025

Page Last Reviewed/Updated Wednesday, August 06, 2025